Do you think you pay 0% fees abroad with your Swiss card?

In reality, you almost always pay… without seeing it.

Most banks in Switzerland do not clearly display their foreign exchange fees.

Instead, they use a much more discreet lever: the exchange rate.

👉 The result:

Even without visible fees, you can lose 1% to 2.5% on every payment in a foreign currency.

And the problem is that this cost is difficult to identify:

- it does not appear as a separate fee line

- it is built directly into the amount charged

- and it is almost impossible to compare without doing the math

Some banks talk about “free payments abroad.” In practice, this only refers to visible fees. The cost is still there, but it is hidden in the rate applied.

In this article, you will understand where the fees are really hidden, how banks apply them, and above all how to avoid paying too much when making payments abroad.

Why foreign exchange fees remain unclear in Switzerland

In Switzerland, foreign exchange fees are among the hardest costs for customers to understand. Unlike account fees or fixed commissions, they are almost never presented clearly.

The issue is that the main cost does not appear as a visible fee. It is built directly into the exchange rate applied during the conversion.

📊 In practical terms, when you make a payment in a foreign currency:

- you pay in EUR, USD, or another currency

- the bank converts the amount into CHF

- but it applies a rate that is slightly less favorable than the market rate

This difference represents the bank’s margin, and therefore the real cost for the customer.

⚙️ With traditional banks, this mechanism is rarely explained in detail. The customer only sees the final amount charged, with no clear indication of the rate applied or the margin included.

💡 By contrast, some neobanks such as Alpian, Neon, or Yuh display more explicit fees, often as a percentage. This makes the cost easier to understand, even if it is still there.

In the end, two banks may appear to offer similar conditions, while the real cost can be very different.

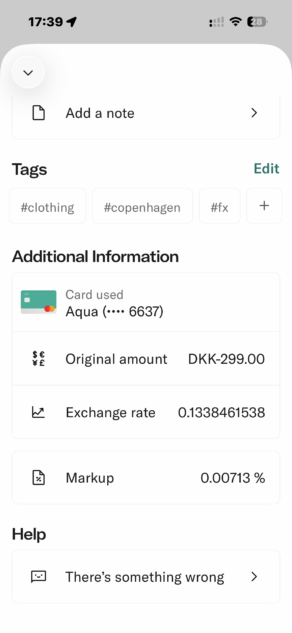

The exchange rate: the main hidden cost

When you pay in a foreign currency, the cost usually does not come from a visible fee, but from the exchange rate applied by your bank.

To understand this, you need to distinguish between two elements: the market rate (often called the interbank rate) and the rate actually used for the transaction. The difference between the two is the margin applied.

📊 Simple example:

- market rate: 1 EUR = 0.96 CHF

- payment of 1,000 EUR → 960 CHF

If the bank applies a less favorable rate:

- amount charged: 975 CHF

The difference of 15 CHF represents a cost of about 1.56%, without any fee being displayed.

⚙️ This mechanism is difficult to detect because:

- no fee appears separately

- the amount is charged directly in CHF

- the rate applied is not always detailed

💡 This is also what makes some offers misleading. A bank can advertise “0% fees abroad” while still applying a margin in the exchange rate.

With traditional banks, this margin is often higher and less visible. Swiss neobanks generally take a more transparent approach, with declared fees or a rate close to the market.

In the end, two cards can display “0% fees” while having a very different real cost.

👉 Key takeaway

The exchange rate is the main lever used to charge for payments in foreign currency. Even without visible fees, a margin is almost always applied.

➡️ And that is exactly what makes these fees hard to identify without doing the math.

Traditional banks vs. neobanks: very different approaches

In Switzerland, not all banks charge foreign exchange fees in the same way. The difference is especially visible between traditional banks and neobanks.

With traditional banks such as UBS, Raiffeisen, or cantonal banks, the fees are usually built directly into the exchange rate. The customer sees a final amount, with no details about the margin applied. On top of that, foreign currency fees are often added, which further increases the total cost.

📊 In practical terms, this model is characterized by:

- fees that are not very visible in the app

- an exchange rate that is rarely detailed

- margins that are often higher

⚙️ By contrast, neobanks usually take a more transparent approach. Providers such as Alpian, Neon, or Yuh generally announce their fees as a percentage or use a rate close to the market.

In some cases, this transparency goes even further. For example, in the N26 app, the amount in foreign currency, the exchange rate, and the margin applied are clearly shown for each transaction. This level of detail makes it possible to understand the true cost of a payment abroad.

Swiss neobanks such as Alpian or Yuh are generally more transparent than traditional banks, even if they do not always show as much detail as some international solutions.

💡 There are, however, intermediate cases. Zak, for example, clearly displays its foreign exchange fees (around 2.5%), but remains relatively expensive. This shows that good transparency does not automatically mean a better price.

In the end, three approaches coexist in Switzerland:

- traditional banks: fees are not very visible and are often high

- neobanks: fees are more transparent and generally lower

- hybrid models: fees are clear, but not always competitive

Alpian Promo Code: ALPNEO – Get 120 CHF

Alpian Promo Code: ALPNEO – Get 120 CHF

Don’t have an Alpian account yet? Use the promo code ALPNEO before June 30, 2026 to get 120 CHF in bonus 🙌

How does the bonus work?

– 55 CHF after depositing at least 500 CHF.

– Up to 65 CHF in investment fee credits.

✅ The Alpian account is free and multi-currency (CHF, EUR, USD, GBP), with an optional Metal Visa Debit card.

Get 120 CHF with Alpian ➡️

Visible fees… and the ones that are not

When you use your card abroad, not all fees are presented in the same way. Some are clearly stated, while others are built into the calculation without being visible.

📊 Visible fees are the easiest to identify. These generally include:

- foreign currency payment fees (often between 1% and 2.5%)

- withdrawal fees abroad

- sometimes fixed fees per transaction

These costs appear in pricing terms and can be compared quickly.

⚙️ But in practice, they only represent part of the real cost. The main part often lies in the exchange rate applied.

This cost is harder to spot:

- it does not appear as a separate fee line

- it is built directly into the amount charged

- it is not always detailed in banking apps

💡 With traditional banks, this invisible part is often the most important. A margin of 1.5% to 2.5% may be built into the rate, with no clear indication.

By contrast, some neobanks make these costs more explicit, with clearly stated fees. The conversion percentage is generally announced, making the real cost easier to understand.

In the end, focusing only on visible fees can give an incomplete picture. Two cards may show low fees while having a very different total cost.

The role of Visa and Mastercard networks

When you pay abroad, your bank is not the only party involved. Payment networks such as Visa and Mastercard play a central role in currency conversion and directly influence the final amount.

In practical terms, the conversion happens in two steps. The network first applies an exchange rate, then the bank may add its own conditions.

📊 The key point is that these networks use their own rates:

- close to the market, but not identical to the interbank rate

- updated daily

- slightly different between Visa and Mastercard

- This means that even without a bank margin, the applied rate is not exactly the one you see on Google.

⚙️ Then, each bank applies its own logic:

- some use the network rate directly

- others add an extra margin

- others combine rate + fees in parallel

This combination determines the real cost.

💡 Some neobanks stay very close to the market rate, with little extra adjustment. Other institutions apply a wider spread.

In the end, two cards using different networks may produce slightly different results, even for the same payment.

Why it is still difficult to compare banks

Comparing foreign exchange fees between banks in Switzerland may seem simple at first. In reality, the differences become clear as soon as you look more closely.

The first problem is that banks do not present their fees in the same way. Some show a clear percentage, while others emphasize the absence of visible fees. In practice, these approaches do not allow a direct comparison between two offers.

📊 Then, several parameters influence the real cost:

- type of card (debit or credit)

- network used (Visa or Mastercard)

- payment currency

- country where the transaction takes place

A simple change in context can affect the final cost, without it being obvious to the customer.

⚙️ The timing of the transaction also matters. The rate applied depends on when the conversion takes place. Two similar payments can therefore result in slightly different amounts.

💡 Specific use cases also matter. With Yuh, for example, already holding EUR allows you to avoid conversion fees. This type of case generally does not appear in standard comparisons.

In the end, two banks may look similar on paper but produce different results in practice. That is why reliable comparisons often rely on simulations or concrete examples.

👉 Key takeaway

Comparing only the displayed fees is not enough. The real cost depends on several variables, which makes comparisons more complex than they seem.

How platforms like Moneyland estimate real costs

To compare foreign exchange fees between banks, some platforms use simulations rather than real transactions. The idea is simple: recreate a specific case, then apply each bank’s conditions.

In practice, this often relies on an example such as a payment of 1,000 EUR converted into CHF. All banks are then evaluated in that same scenario, which makes the results comparable.

Platforms such as Moneyland, which regularly publishes studies on foreign payments in Switzerland, use exactly this type of method to build their rankings.

👉 These analyses are based on standardized simulations, allowing banks to be compared under identical conditions.

The calculation does not only include displayed fees. It also incorporates an estimate of the exchange rate in order to approximate the real cost of a payment in a foreign currency.

⚙️ However, this is a theoretical model. The results are consistent, but may vary in practice depending on the timing of the transaction, the currency used, or how you use your account.

In reality, several factors can change the cost. The timing of the transaction, the currency used, and how you use your account all play a role. For example, with Yuh, already holding EUR allows you to avoid conversion fees, which is generally not taken into account in this type of simulation.

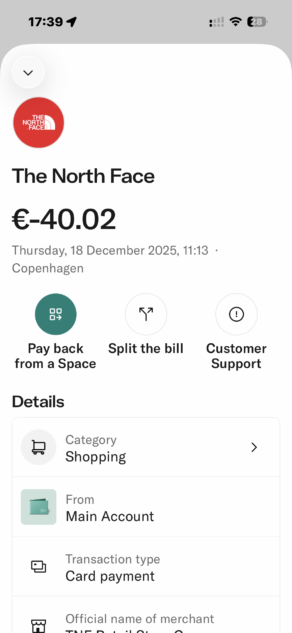

Concrete example: how much does a payment abroad really cost?

Foreign exchange fees remain abstract… until you look at a concrete example.

Let’s take a simple case: a payment of 1,000 EUR with a Swiss card.

On paper, the amount should match the market rate. In practice, the result can vary significantly depending on the bank used.

👉 Here is what that looks like in a typical scenario:

- traditional banks: around 975 to 985 CHF charged

- neobanks such as Neon: around 965 to 975 CHF

- Yuh: around 969 CHF (with 0.95% conversion)

- Alpian: close to 960 to 965 CHF

| Bank | Amount charged (for 1,000 EUR) | Estimated fees | Transparency |

|---|---|---|---|

| Alpian | 960–965 CHF | ~0% to 0.2% | Very high |

| Neon | 965–975 CHF | ~0.5% to 1% | High |

| Yuh | ~969 CHF | 0.95% | Very high |

| Zak | ~985 CHF | 2.5% | High |

| Traditional banks (UBS, Raiffeisen) | 975–985 CHF | 1.5% to 2.5% | Low |

The difference may seem small for one transaction, but it becomes significant over a trip or with regular use.

⚙️ What explains these differences:

- the margin built into the exchange rate

- foreign currency fees

- each bank’s pricing structure

💡 In some cases, the cost can even be reduced to zero. For example, with Yuh, if you already hold EUR in your account, there is no conversion.

In the end, two cards may display similar conditions but produce a very different result in practice.

👉 Key takeaway

A payment abroad can cost between 0% and more than 2.5% depending on the bank. The difference does not always come from visible fees, but mainly from the exchange rate applied.

YUH Promo Code: YUHNEO

Don't have a YUH account yet? Use our referral code to open your free YUH Bank account!

Use the promo code YUHNEO before June 30, 2026 to receive a bonus of 50 CHF in Trading Credits + 5 CHF (250 SWQ) for FREE 🙌

Get 55 CHF Free with YUH ➡️

How to avoid hidden foreign exchange fees

Once you understand where the real fees are, it becomes easier to avoid them. In most cases, it is not the visible fees that cost the most, but the rate applied.

The first rule is to pay in the local currency. When a terminal offers to charge you in CHF abroad, it often applies an unfavorable rate. Accepting the local currency usually gives you a better rate.

📊 The choice of bank also plays an important role. Some neobanks offer conditions that are closer to the market, with more transparent fees.

⚙️ It is also possible to optimize further depending on how you use your account. For example, with Yuh, already holding EUR in your account avoids any conversion. In that case, foreign exchange fees disappear completely.

💡 Finally, it is useful to keep a simple approach: compare the amount actually charged in CHF rather than relying only on the fees displayed. This is often the only way to see the real cost.

In the end, avoiding hidden fees does not require complex calculations, but rather understanding how they are applied and adopting the right habits when paying.

👉 Key takeaway

Foreign exchange fees can be reduced, or even avoided, by following a few simple best practices. The choice of bank and the way you pay make all the difference.

Conclusion: clearer fees… and often lower costs

Foreign exchange fees in Switzerland are not always easy to identify. In many cases, they do not take the form of a visible fee, but of a difference in the exchange rate applied.

This explains why two banks can display similar conditions while producing very different results in practice.

Traditional banks often remain less transparent on this point, with margins built into the rate. By contrast, neobanks such as Alpian, Neon, or Yuh generally offer a clearer approach, with visible fees or rates close to the market.

📊 In most cases, this also translates into lower costs, especially for payments abroad.

Choosing the right bank then depends on how you use it. Some people prioritize simplicity, while others want to optimize every transaction. But in all cases, understanding how foreign exchange fees work helps you avoid paying too much.

Alpian Promo Code: ALPNEO – Get 120 CHF

Don’t have an Alpian account yet? Use the promo code ALPNEO before June 30, 2026 to get 120 CHF in bonus 🙌

How does the bonus work?

– 55 CHF after depositing at least 500 CHF.

– Up to 65 CHF in investment fee credits.

✅ The Alpian account is free and multi-currency (CHF, EUR, USD, GBP), with an optional Metal Visa Debit card.

Get 120 CHF with Alpian ➡️

Frequently Asked Questions (FAQ) about foreign exchange fees in Switzerland

✅ Do Swiss banks charge fees for payments abroad?

Yes, in most cases. Even when the fees are not visible, part of the cost is often built into the exchange rate applied during the conversion.

This means you may pay more without seeing a specific fee line on your statement.

✅ What is the real cost of a payment in a foreign currency?

In practice, the cost usually ranges between 1% and 2.5%, depending on the bank. This amount mainly depends on the margin applied to the exchange rate, as well as any additional fees.

So two banks may display low fees while having a very different real cost.

✅ Why are foreign exchange fees difficult to compare?

Banks do not present their fees in the same way. Some show a clear percentage, while others build the costs directly into the exchange rate.

This makes comparisons complex unless you analyze the amount actually charged in CHF.

✅ Should you pay in CHF or in the local currency abroad?

It is generally recommended to pay in the local currency. When a terminal offers payment in CHF, it often applies a less favorable conversion rate.

Paying in the local currency usually gives you a better rate in most cases.

✅ Are neobanks really cheaper for payments abroad?

In most cases, yes. Neobanks often use exchange rates that are closer to the market and display more transparent fees.

This helps reduce the total cost, even though fees may still exist depending on usage.

✅ Can you avoid foreign exchange fees completely?

Yes, in some cases. For example, if you already hold the foreign currency in your account (EUR or USD), no conversion is needed.

However, in most situations, a conversion takes place and comes with an associated cost.

Philippe is the founder of Neo-banques.ch, a website specializing in the analysis of Swiss online banks and neobanks. For several years, he has been testing and comparing the main solutions on the market, including Yuh, Alpian, Neon, Zak, Wise, Revolut, and N26, for both personal and professional use. His approach is based on hands-on experience, fee analysis, feature comparison, and the overall quality of the day-to-day user experience.