Managing your money better is not just about tracking your spending. Above all, it means allocating what you earn more effectively between your everyday needs, your savings, your projects and, if your situation allows, your first investments. In practice, this mainly requires an approach that is simple, clear and realistic.

With this in mind, Zak can play a useful role. Banque Cler’s app is not only designed to manage everyday expenses: it can also help you structure certain savings goals, better separate shared projects, integrate your pillar 3a pension savings and, for some users, start investing with Zak Invest.

In this article, we will look at how to organize your money better step by step, and then to what extent Zak can be integrated into this process in practical day-to-day use.

Why managing your money better has become essential

Managing your money better is not only about tracking your expenses. It is also a way to keep more control over your daily life, avoid certain mistakes and prepare your projects more effectively.

Today, many people feel that their money disappears quickly between fixed costs, everyday spending and unexpected expenses. Even with a stable income, it is not always easy to know how much is really left at the end of the month, how much can be saved and from what point it becomes reasonable to start investing.

Organizing your finances better helps you see things more clearly and make better decisions. The goal is not to calculate everything down to the last cent or to follow an overly strict budget, but rather to put in place a simple and realistic structure.

Managing your money better can help you:

- 📊 better understand where your budget goes each month

- 🛟 avoid letting unexpected expenses throw your finances off balance,

- 💰 save more consistently,

- 🎯 prepare your future projects with more peace of mind,

- 📈 build stronger foundations before investing.

This approach is useful even if you are just getting started. Before looking for complicated solutions, it is often more effective to go back to the essentials: knowing what you earn, what you spend and what you can realistically set aside. This is the foundation on which you can then build a more stable way of managing your money.

Start by understanding where your money goes

Before trying to save better or invest, you first need to know where your money actually goes each month. This step may seem simple, but it is often overlooked. Yet without a clear view of your income and your expenses, it becomes difficult to build a realistic budget.

The first thing to do is list your net monthly income, then look at your main expenses. The goal is not to make everything complicated, but to distinguish the main categories that weigh on your budget.

For example, you can divide your finances into three blocks:

| Types of Expenses | Examples |

|---|---|

| Fixed Expenses | Rent, health insurance, phone, subscriptions |

| Variable Expenses | Groceries, transportation, restaurants, leisure activities |

| Occasional Expenses | Vacations, gifts, repairs, unexpected expenses |

This sorting already makes it easier to see what you need to pay every month, what changes depending on your habits and what can throw your budget off balance at certain times of the year.

In many cases, the problem does not come from a single large expense, but from the accumulation of small outflows of money that are barely noticeable on a daily basis. A few forgotten subscriptions, repeated purchases or comfort spending can end up significantly reducing your margin at the end of the month.

Understanding where your money goes helps you:

- 📍 spot the most important spending categories,

- 🔎 identify expenses that can be reduced,

- 💡 more accurately estimate what you can set aside,

- 📅 better anticipate the more expensive months,

- 📈 start from a stronger base to organize your budget.

This step does not need to be perfect to be useful. Even a simple overview can already help you make better decisions. Once you know what comes in and what goes out, it becomes much easier to put in place a consistent budget, and then think about your savings and your first investments.

Set up a simple and realistic budget

Once you have a better understanding of where your money goes, you can move on to the next step: organizing your budget more clearly. There is no need to create a complicated spreadsheet or track every expense down to the last cent. A useful budget should first and foremost be easy to understand and realistic over time.

A common mistake is trying to change everything at once. Cutting your spending sharply, setting an overly ambitious savings target or depriving yourself in every category rarely works for long. In practice, a budget works better when it remains adapted to your pace of life and your monthly obligations.

The easiest approach is to think in terms of broad categories. One part of your money covers everyday expenses, another helps build an emergency fund, and another can be reserved for your future goals, including your first investments.

For example, you can structure your budget around three blocks:

- 🏠 everyday expenses: rent, insurance, groceries, transport, subscriptions,

- 💰 savings: emergency reserve, future projects, safety margin,

- 📈 investments: amounts you choose to allocate gradually with a long-term perspective.

This approach changes the way you manage your money. Instead of spending first and saving only if something is left, you start by defining a clear allocation from the beginning. Even with modest amounts, this helps create a more stable framework.

A simple budget does not need to be perfect to be effective. What matters most is knowing how much you want to allocate to each priority and being able to stick to that structure from one month to the next. Over time, you can then adjust the amounts depending on changes in your income, expenses and projects.

Build an emergency fund before going further

Before thinking about investing, it is generally safer to start with an emergency fund. This reserve is not meant to finance a specific project or seek returns. Its role is simpler: it allows you to absorb an unexpected expense without throwing your entire budget off balance.

A breakdown, an unexpected bill, a medical expense or a change in your situation can quickly put pressure on your finances if you have no margin at all. In that case, you may either have to use money that was intended for other goals or sell an investment at the wrong time.

Having an emergency fund helps create that safety net. It makes it easier to deal with the unexpected without undermining the rest of your financial organization.

In practice, this reserve can help you:

- 🛟 deal with an unexpected expense,

- 📉 avoid having to cash out investments too early,

- ⚖️ maintain more stability in your budget,

- 🧘 move forward with more peace of mind on a daily basis.

The amount you need naturally depends on your situation, your fixed costs and your level of financial security. The idea is not necessarily to build a large sum immediately, but to start gradually and give priority to this foundation before going further.

Once this reserve is in place, it becomes easier to think about medium-term savings and then investing. You then move forward on a stronger base, with a more consistent approach and less risk of having to step back at the first unexpected event.

Define your financial goals

It is difficult to manage your money well if you do not clearly know why you are setting money aside. Saving “when there is something left” or investing “because you probably should” rarely leads to a sustainable structure. By contrast, specific financial goals give clearer direction to your decisions.

Not all goals have the same time horizon. Some concern the next few months, while others stretch over several years. This difference is precisely what helps you allocate your money more effectively.

To allocate your money better, it is useful to distinguish between different time horizons.

| Horizon | Examples of objectives | What to prioritize |

|---|---|---|

| Short term | Emergency fund, vacation, useful purchase | Availability |

| Medium term | Training, personal project, down payment | Balance |

| Long term | Retirement, assets, gradual investment | Long-term vision |

This distinction matters because you will not manage money you need soon in the same way as money you can leave untouched for longer. The shorter your horizon, the more you need stability and accessibility. The longer it is, the more you can think in terms of a different savings or investment approach.

Defining your goals also helps avoid an overly abstract budget. Instead of simply trying to spend less, you start giving your money a role. One part helps secure your daily life, another prepares a concrete project, and another can support a longer-term vision.

Even if your goals change over time, this step already helps you build a more consistent structure. You gain a clearer view of what you want to finance, within what timeframe and with what level of priority.

Find the right balance between spending, saving and investing

Managing your money well does not mean putting everything into savings or investing as quickly as possible. In practice, the goal is rather to find a consistent balance between what you need today, what you want to secure for tomorrow and what you can start building over the long term.

This is often where things become more complicated. Many people hesitate between two opposite instincts: either keeping everything in their account to feel safe, or wanting to invest too quickly without yet having a sufficiently stable base. In both cases, the organization remains incomplete.

To move forward more calmly, it helps to allocate your money according to its function:

- 🛒 what should be used for your everyday expenses,

- 🛟 what should remain available for your emergency savings,

- 📈 what can be dedicated to longer-term goals, including your first investments.

This logic helps avoid mixing everything together. Money that you may need to use quickly should not be managed in the same way as money you are prepared to leave aside for longer. The shorter your horizon, the more flexibility you need. The longer it is, the more you can consider an approach focused on progress and consistency.

The right balance therefore depends less on a universal rule than on your own situation. Your income, your fixed costs, your projects and your risk tolerance directly influence how you can allocate your money. What matters most is avoiding extremes and building an organization you can maintain over time.

In practice, it is often more useful to start modestly, with a clear allocation, rather than waiting for a “perfect moment” that never comes. A simple and well-maintained foundation is generally more valuable than an overly ambitious strategy that is difficult to follow over time.

How Zak can fit into a simpler way of managing your money

Once you have a clearer view of your budget, your savings and your priorities, the challenge is no longer only to track your money, but to organize it better on a daily basis. This is where Zak can have real practical value.

The app is not only useful for managing your everyday spending. It can also help you allocate your money more effectively according to your goals, without leaving everything in one single balance. This type of organization is useful to avoid mixing together the money intended for this month’s expenses, the money you want to keep aside, or certain sums planned for specific projects.

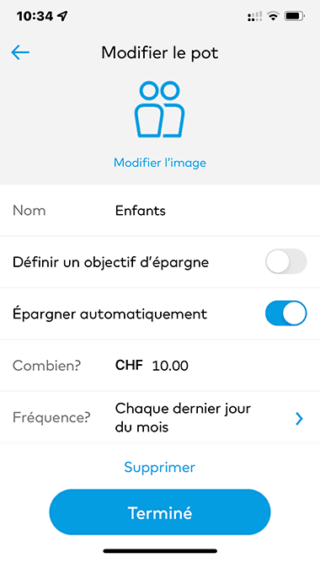

The savings pots are part of that logic. They allow you to set money aside for different goals, such as an emergency reserve, a trip, a major purchase or simply an amount you would rather not touch. They also make it possible to save automatically, which can help you stay consistent over time. It is a simple way to make your budget easier to read and to see more clearly how much money you are setting aside.

Zak also offers shared pots, which can be useful if you manage certain expenses with a partner or with others. This may apply to a couple, a flatshare or a shared project. The main advantage is being able to better separate what belongs to your personal expenses from what relates to shared spending.

Zak’s usefulness can also go further with pillar 3a pension savings. Instead of managing your account, your savings and your retirement in completely separate environments, you can integrate this dimension into a more consistent financial organization.

| Function | What are the practical benefits? |

|---|---|

| Savings accounts | Setting aside money for specific goals without mixing everything together |

| Common funds | Better managing certain expenses when sharing with others |

| Retirement savings plan 3a | Integrating retirement planning into your financial strategy |

| Investment | Linking daily management with gradual investing |

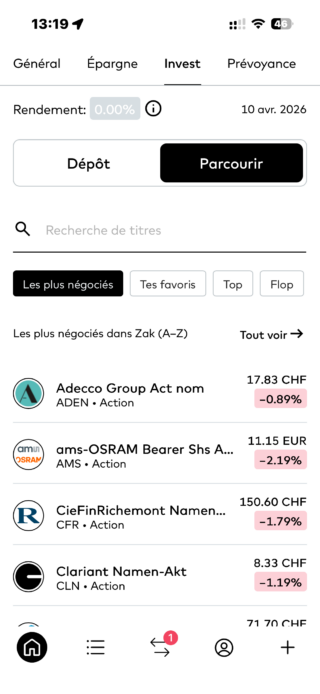

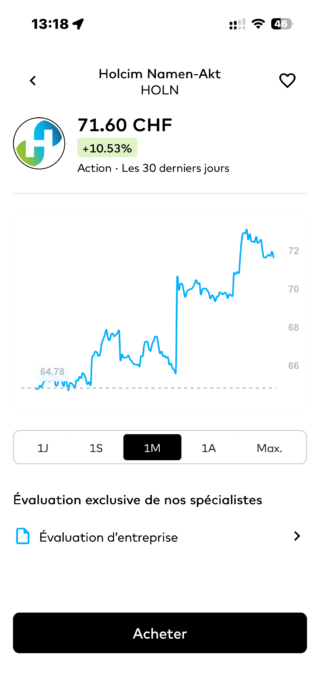

Finally, if you want to go a step further, Zak Invest can be a logical next step. The goal is not to start investing too quickly, but to make it easier to move from everyday money management to a more gradual approach to saving and investing. Having this option within the same environment can also make the transition simpler for users who are just getting started.

Ultimately, the benefit of Zak is not that it replaces the basics of good financial management. Rather, it can make those basics easier to apply: better separate your priorities, structure your money more clearly and move step by step between budget, savings, pillar 3a and investing.

ZAK Promo Code: NEOZAK

ZAK Promo Code: NEOZAK

Don't have a Zak Bank account yet? Use our referral code to open your free ZAK Bank account!

Use the promo code NEOZAK before June 30, 2026 to get 50 CHF for FREE 🙌

Get 50 CHF with Zak Bank ➡️

Start investing gradually with Zak Invest

Once you have set up a clear budget, built an emergency fund and defined your financial priorities, you can start thinking about investing under better conditions. This is where Zak Invest can find its place.

The point is not to invest quickly or try to do “better” from the outset. What matters most is moving forward with an approach you understand, that you can maintain over time and that remains consistent with your situation.

In this context, Zak Invest can help you take your first steps without multiplying tools or platforms. You stay in the same environment to manage your day-to-day finances, track your savings and, if you wish, start investing gradually. This simplicity can be an advantage for people who want to get started with a more accessible and consistent approach to managing their money.

That does not mean you should invest without thinking. Before getting started, it is better to keep a few simple principles in mind:

- 💵 invest only money you do not need in the short term,

- 📉 start with a reasonable amount,

- 📅 move forward with a certain level of consistency,

- 📈 keep a long-term mindset,

- 🧭 choose investments suited to your profile and your risk tolerance.

If you are just starting out, ETFs, for example, can offer a simpler approach to understand than buying several individual stocks. Depending on your level of knowledge, you may also prefer a more cautious approach at first, starting modestly and observing how your strategy evolves over time.

So the main goal is not to seek immediate returns. Rather, it is about integrating Zak Invest into a more consistent process: first manage your money better, then create savings capacity, and finally begin investing progressively, with a method you can realistically maintain over time.

Mistakes to avoid when trying to manage your money better

Managing your money better does not only depend on the good habits you put in place. It also means avoiding certain mistakes that come up frequently, especially when reorganizing your budget, starting to save or taking your first steps in investing.

The first mistake is trying to change everything at once. Drastically cutting your spending, setting overly ambitious goals or wanting to invest immediately may feel motivating at first, but this type of approach rarely lasts. Stronger financial management is generally built progressively.

Another common mistake is wanting to invest without having built an emergency fund. As long as you have no margin for unexpected expenses, even a small problem can force you to use money intended for other goals or sell an investment at the wrong time.

It is also common to underestimate certain small recurring expenses. Individually, they seem harmless. Added up over several weeks or months, however, they can significantly reduce your ability to save.

Here are some mistakes to avoid as a priority:

- ⚠️ trying to set up a budget that is too strict,

- 🛟 starting to invest without an emergency reserve,

- 🧾 neglecting small expenses that accumulate,

- 📉 changing your strategy every time the market falls,

- 🎯 moving forward without a clear financial goal.

Finally, many people give up too quickly because they are looking for immediate results. In reality, managing your money better often relies on simple adjustments repeated over time. The goal is not to be perfect from the beginning, but to avoid the mistakes that weaken your organization and to build something more consistent month after month.

Let your financial organization evolve over time

Good money management is never completely fixed. What works today may not necessarily be suitable in a year, especially if your income, your expenses or your priorities change. The goal is therefore not to build a perfect system from the start, but an organization simple enough to be adjusted over time.

At first, your priorities are often very practical: tracking your spending better, finding a bit more margin at the end of the month or building an initial emergency fund. Later on, other goals may become more important, such as a personal project, pillar 3a pension savings or your first investments.

What matters is regularly reviewing a few basic points:

- 📌 is your budget still suited to your current situation,

- 💰 has your savings capacity increased or decreased,

- 🎯 are your financial goals still the same,

- 📈 is the portion dedicated to investing still consistent with your time horizon and your risk tolerance.

This update does not need to be complicated. In many cases, a quick review is enough after a significant change: an increase or decrease in income, a new project, a move, higher-than-expected expenses or a change in your family situation.

Over time, you may also choose to structure certain priorities more clearly. For example, strengthening your available reserve, contributing more regularly to your pillar 3a, or allocating a clearer share to your investments with Zak Invest, if your budget and your time horizon allow it.

The main thing is that your organization continues to match your reality, rather than a plan set once and for all. In other words, managing your money better is not only about putting strong foundations in place, but also about adjusting them at the right pace.

Conclusion

Managing your money better does not necessarily require a complicated method. In most cases, it simply means putting clear foundations in place: tracking your spending better, maintaining an emergency fund, defining your priorities and moving forward gradually based on your situation.

In this process, Zak can be a useful everyday tool. The app can help you organize your money better, separate certain savings goals, manage shared expenses, integrate your pillar 3a pension savings and, if you wish, take your first steps with Zak Invest.

The key point is not to change everything at once, nor to look for a perfect structure from the beginning. What is usually most useful is to put in place a simple framework that you can realistically maintain over time.

In the end, managing your money better with Zak mainly means giving each amount a clearer purpose, so you can move forward more consistently between budget, savings, retirement planning and investing.

ZAK Promo Code: NEOZAK

Don't have a Zak Bank account yet? Use our referral code to open your free ZAK Bank account!

Use the promo code NEOZAK before June 30, 2026 to get 50 CHF for FREE 🙌

Get 50 CHF with Zak Bank ➡️

Frequently asked questions (FAQ) about managing your finances with Zak

✅ How can you manage your money better with Zak?

Managing your money better with Zak first means organizing your budget, your savings and your financial goals more effectively. The idea is not only to track your spending, but also to allocate your money more clearly between everyday life, unexpected expenses and future projects.

Zak can fit into this approach thanks to tools such as savings pots, shared pots, pillar 3a pension savings and, if you want to go further, starting to invest with Zak Invest.

✅ Should you save first before investing with Zak?

Yes, in most cases, it is better to start by building an emergency fund before investing. This reserve helps you deal with unexpected expenses without having to sell an investment at the wrong time.

Once this foundation is in place, it becomes easier to consider solutions such as Zak Invest in a more gradual way.

✅ What are savings pots in Zak used for?

Savings pots let you set money aside for specific goals, such as an emergency fund, a trip or a major purchase. They help you avoid mixing everything into one single balance and can also be used to save automatically on a more regular basis.

✅ Can you manage a project or shared expenses with Zak?

Yes, Zak also offers shared pots, which can be useful for certain expenses involving several people. This may apply to a couple, a flatshare or a shared project.

The benefit is being able to separate personal expenses and shared expenses more clearly.

✅ Does Zak also allow you to prepare for retirement?

Yes, Zak also lets you integrate pillar 3a pension savings into your financial organization. This can be useful if you want to structure your long-term savings more effectively and avoid treating retirement separately from the rest of your finances.

Pillar 3a can therefore become part of a broader approach that includes budget, savings and long-term goals.

✅ Is Zak Invest suitable for getting started with investing?

Zak Invest may be suitable for people who want to take their first steps in investing gradually. The approach can be interesting if you want to stay within the same ecosystem to manage your money, save and invest.

As always, it remains important to invest only money you do not need in the short term and to choose investments suited to your profile.

✅ How can you start investing gradually with Zak Invest?

The simplest way is to start with a reasonable amount, invest with a certain level of consistency and keep a long-term mindset. There is no need to move too fast or look for immediate returns.

Before using Zak Invest, it is generally better to have a clear budget, an emergency fund and defined financial goals.

✅ Can you use Zak without investing right away?

Yes, absolutely. Zak can already be useful for managing your budget better, organizing your savings and structuring certain financial goals, without moving straight into investing.

For many people, the first step is simply to track their money better on a daily basis before going further.

✅ What is the difference between saving and investing with Zak?

Saving means keeping money available for short- or medium-term needs, such as an unexpected expense or a specific project. Investing means putting part of your money to work over a longer period, with a certain level of risk.

With Zak, these two approaches can fit into a simpler organization, provided you clearly distinguish between the money that should remain available and the money you can leave invested for longer.

✅ Can Zak help you organize your budget better on a daily basis?

Yes, Zak can help you organize your money better on a daily basis by bringing several dimensions together in the same environment: everyday expenses, goal-based savings, shared pots, pillar 3a and investing.

The main benefit is making your financial organization more readable and easier to follow over time.

Philippe is the founder of Neo-banques.ch, a website specializing in the analysis of Swiss online banks and neobanks. For several years, he has been testing and comparing the main solutions on the market, including Yuh, Alpian, Neon, Zak, Wise, Revolut, and N26, for both personal and professional use. His approach is based on hands-on experience, fee analysis, feature comparison, and the overall quality of the day-to-day user experience.