For eight years, Swiss savers faced negative interest rates, which meant that their money earned them nothing or even cost them. This situation was due to the 2008 crisis, which led central banks to cut interest rates to stimulate the economy. In Switzerland, the Swiss franc strengthened, raising concerns for the export industry and prompting the Swiss National Bank (SNB) to introduce negative interest rates to encourage spending rather than investment. saving.

But the situation has changed recently due to the current inflationary environment. Since 2022, the US and European central banks have started to raise their interest rates and the SNB did the same last September. As a result, since the beginning of this year, Swiss banks have resumed recommending the savings accounts of their customers.

In 2023, neobanks and online banks reacted quickly by offering better interest rates to attract new customers.How to take advantage of higher interest rates in Switzerland

Here are the possible options to take advantage of the higher interest rates in Switzerland:

- Private online account: neobanks (online banks) in Switzerland can offer competitive interest rates on their private accounts, this is the case of Zak Bank for example. See the charts below for rates.

- Traditional savings accounts: Swiss banks have raised interest rates on their traditional savings accounts, offering better yield opportunities.

- Online savings accounts: Neobanks in Switzerland can also offer more competitive interest rates on their savings accounts.

- Cooperative banks: The cooperative banks in Switzerland have also increased the interest rates on their savings accounts.

It is important to note that interest rates may vary from bank to bank and may be subject to specific conditions.

Changing banks for a better interest rate?

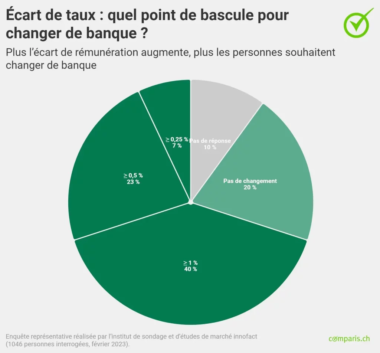

According to a survey carried out by comparator Comparis, around a quarter of Swiss savers plan to transfer their money to another bank because of interest rates. This dissatisfaction is mainly linked to the fact that more than half of savers (54%) only receive an interest rate of 0.25% or less on their deposits.

Source: Comparis. 40% of savers would leave their bank if another bank’s interest rate were at least 1% higher

Those aged 18-35 are the most likely to switch banks: with 33% planning to transfer their funds elsewhere. The 36 to 55 age groups follow closely with 26%, while only 17% of people over 56 expect to change their financial institution.

Romands are more determined to switch banks, with 33% planning to close their savings account this year and switch to a bank offering more attractive interest rates, compared to 24% % for German-speaking Switzerland (German-speaking region) and 10% for Ticino. City dwellers are also more inclined to change than rural dwellers, at 30% versus 18%.

Interest rates for private accounts in Switzerland in June 2026

In June 2026, only Swiss neobanks offer interests on private accounts:

| Neobank | Interest Rate | Interest Cap | Withdrawal Limit |

|---|---|---|---|

| Alpian | 0.15 % | Above 125,000 CHF. 0.01 % below. | None |

| Neon | 0.00 % | - | None |

| Yuh Bank | 0.00 % | - | None |

| Zak | 0.05 % | Up to CHF 25,000 | None |

Savings account interest rates of large swiss banks in June 2026

| Bank | Interest Rate | Interest Cap | Withdrawal Limit |

|---|---|---|---|

| Banque Cantonale Vaudoise (BCV) | 0,00 % | - | Up to CHF 10,000 per month |

| Zürcher Kantonalbank (ZKB) | 0,00 % | - | Up to CHF 10,000 per year |

| Migros Bank | 0,00 % | - | Up to CHF 50,000 per month |

| PostFinance | 0,00 % | - | Up to CHF 100,000 per year |

| Raiffeisen | 0,00 % | - | Up to CHF 20,000 per month |

| UBS | 0,00 % | - | Up to CHF 50,000 per year |

The interest rates offered by Swiss banks in this table are now 0.00%, reflecting the trend of extremely low rates in the Swiss market in 2025. No interest is currently offered, even for limited deposit amounts. This highlights the challenge for savers seeking returns through traditional bank accounts. In this context, neobanks or online platforms, which may offer symbolic interest rates or additional attractive services, could prove more appealing for optimizing savings management.

Private account or savings account?

Savings accounts have higher interest rates than private accounts, although interest rates may vary each month.

However, it is important to take into account the costs associated with savings accounts, such as the annual maintenance fee or the closing fee account strong>. In addition, the maximum interest rates on savings accounts are often applicable up to a certain capped amount. Beyond this amount, the interest rate may be lower, or even zero.

We therefore wanted to take a closer look at what one of them offers: Zak

A private account interest rate of 0.05% at Zak

Several neobanks have already raised interest rates on their private accounts.

This is the case of Zak, which currently offers you a interest rate of 0.05% on your Zak private account., up to CHF 25,000.

This means that it is not necessary to block your money in Savings pots to benefit from interest of 0.05%. You continue to have your money while being paid.

This flexibility offered by Zak is not available from the major Swiss banks: you can therefore consider using Zak as a private account and PostFinance or a cantonal bank for your savings greater than CHF 25,000, for example.

ZAK Promo Code: NEOZAK

ZAK Promo Code: NEOZAK

Don't have a Zak Bank account yet? Use our referral code to open your free ZAK Bank account!

Use the promo code NEOZAK before June 30, 2026 to get 50 CHF for FREE 🙌

Get 50 CHF with Zak Bank ➡️

Philippe is the founder of Neo-banques.ch, a website specializing in the analysis of Swiss online banks and neobanks. For several years, he has been testing and comparing the main solutions on the market, including Yuh, Alpian, Neon, Zak, Wise, Revolut, and N26, for both personal and professional use. His approach is based on hands-on experience, fee analysis, feature comparison, and the overall quality of the day-to-day user experience.